Ask the Expert: Avoiding mistakes when diversifying retirement savings into shares

Diversification is a good idea to reduce the overall risk of your superannuation. But if you aren’t confident about shares here’s what to do, according to Craig Sankey.

Question 1

My wife and I are aged 70. We have a self-managed super fund, which only has real estate assets plus a small cash deposit of $200,000, which I would like to invest in shares (for diversification purposes).

As I know nothing about the sharemarket, I would like to invest this money into a major super fund. However, I’m having trouble finding one that accepts deposits and membership from an SMSF.

Can you please steer us in the right direction?

Diversification is a good idea. This helps reduce the overall risk of your superannuation portfolio.

Similarly, if you are not confident about shares yourself, using a professional fund manager is also a good idea.

Self-managed super funds (SMSFs) are the investment structure, and not generally a type of super fund that can invest in another fund.

However, a handful of super fund providers do allow SMSF trustees to access specific assets or investment expertise from their platforms.

I’m not aware of all the super funds that offer this. As I work with industry super funds, I am aware that Hostplus has a specific solution that may suit your SMSF. Details can be found here.

Question 2

I am an 85-year-old woman. I have superannuation, with my two children listed as beneficiaries for when I pass on.

When I do, will it be 30 per cent tax taken or 15 per cent?

If you leave your super to a non-dependant, which includes adult children that are not financially dependent on you, then the rate of tax depends on the components within your super fund.

There are three possible components:

Tax-free component

As the name suggests, this payment is always paid tax free, regardless of who it gets paid to.

If you have previously made after-tax (non-concessional) contributions to super, then they would have been added to this component.

Taxable component – taxed element

This component is taxed at 15 per cent plus Medicare (2 per cent).

Generally, this is the largest component for most people. Employer super guarantee contributions, salary sacrifice and earnings within accumulation are added to this component.

Taxable component – taxed element

Stay informed, daily

This is taxed at 30 per cent plus Medicare.

This component may come about if you were a member of an untaxed super fund or if the proceeds of the death benefit are sourced from life insurance within super (unlikely in your circumstances).

Your super fund will be able to explain what your tax components are. If it is a goal to leave the funds tax free to your adult children, you should look to obtain some financial or estate planning advice.

Question 3

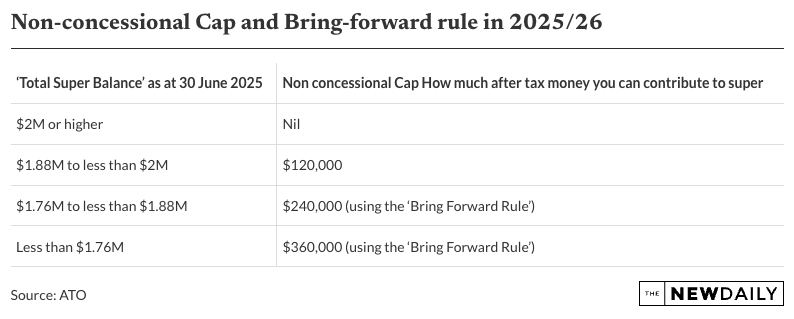

Next financial year, I plan to put $360,000 into my super, using the bring forward rule.

Does it have to be deposited in one hit or can it be done in several deposits over the full financial year?

The “bring forward rule” is when you make after-tax non-concessional contributions into super and you want to use the current and future non-concessional caps.

The current annual cap is $120,000. Depending on your total super balance, you can bring forward up to two future years, therefore making $360,000 in after tax contributions.

As soon as you exceed the annual cap of $120,000, the bring forward rule automatically triggers (if eligible). You don’t need to notify anyone. The ATO keeps track of this.

The total of $360,000 can be made in one go, over various contributions in year one, two and three. Or any combination.

For example, let’s say you add $200,000 this financial year. You have triggered the bring forward. You can make the remaining $160,000 also in this financial year, or the following, or in year three.

It’s important not to exceed the $360,00 over that three-year period, as penalties apply. You also need to ensure you are eligible to contribute based on your total super balance, as shown in the table below.

Craig Sankey is a licensed financial adviser and head of Technical Services and Advice Enablement at Industry Fund Services.

Disclaimer: The responses provided are general in nature, and while they are prompted by the questions asked, they have been prepared without taking into consideration all your objectives, financial situation or needs.

Before relying on any of the information, please ensure that you consider the appropriateness of the information for your objectives, financial situation or needs. To the extent that it is permitted by law, no responsibility for errors or omissions is accepted by IFS and its representatives.

Want to see more stories from InDaily Qld in your Google search results?

- Click here to set InDaily Qld as a preferred source.

- Tick the box next to "InDaily Qld". That's it.