Ask the expert: Super or mortgage? Priorities when approaching retirement

Salary sacrifice can be a financially advantageous move as you near retirement, even if you still have a mortgage to pay off.

Question 1

I was talking to a life-long friend yesterday. She will work another five years through to 70, as she has a mortgage.

She is salary sacrificing $100 a week into her super, but will never have enough to be fully self-funded.

Considering that last point, wouldn’t she be better off knocking the mortgage over quicker and then focusing on her super balance?

I don’t know the details of your friend, so can only provide some high-level observations.

Given her age, 65, salary sacrifice may be the appropriate strategy. She would be saving on income tax with such an arrangement.

The higher her marginal tax rate, the more she saves. Given her age, she can access her super at any time, so there’s no real downside.

The above assumes she is still comfortably meeting her ongoing loan repayments.

Once she does retire, she can take money out of super tax-free to pay out the loan. In fact, as she is 65, she can do that at any time.

You might like

Your comment “but will never have enough to be fully self-funded”, needs to be put in context.

“Self-funded” is not a black and white outcome, it’s a continuum. Most people today are partially self-funded. That is, they have some super (and potentially non-super assets) and still receive some age pension.

Having some super income to top up your age pension makes a big lifestyle difference for many retirees.

Question 2

Please explain the bring forward rule for non concessional contributions.

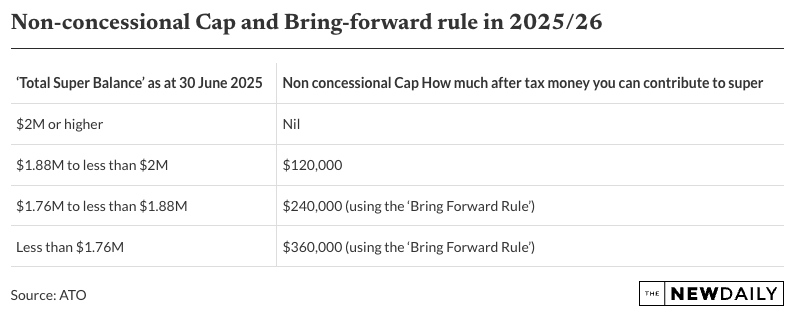

The bring forward rule is in relation to the superannuation non-concessional cap.

Because superannuation tax rules are so generous, there are limits on how much you can put into super each year.

There is a separate cap for pre-tax contributions (concessional cap) and after-tax contributions (non-concessional cap). For the 2025-26 financial year, the annual cap for non-concessional contributions is $120,000.

The bring forward rule is for eligible individuals under 75 to access up to three years’ worth of contributions ($360,000 for 2025/26) in one year, triggered automatically when exceeding the annual cap.

This recognises that sometimes people receive a large amount of money (sale of an asset, inheritance etc).

Eligibility depends on their age, total super balance and previous contributions.

In effect you are “bringing forward” your future allowable contribution, whilst still staying under the contribution cap amounts.

Stay informed, daily

The below table shows how much “bring forward” you can use, depending on your “total super balance” as at the previous June 30.

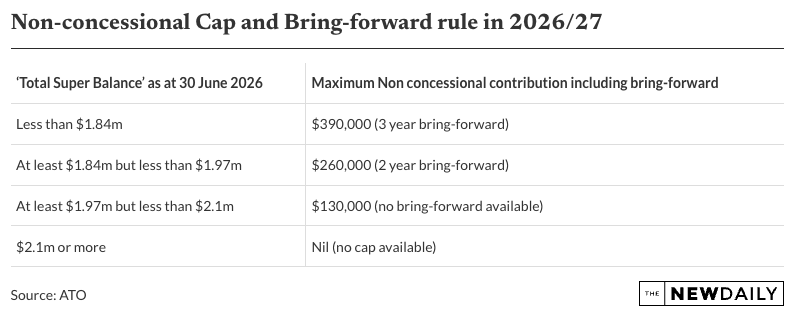

Note, the total super balance threshold and superannuation contribution caps (including the bring forward amount) will be indexed for 2026-27.

Please see below:

Note, the increase to the non-concessional cap in 2026-27 will not apply to individuals who have already triggered the bring- forward rule in either 2025-26 or 2024-25 and are still in their bring forward period in 2026-27.

Question 3

I retired early and have recently gone back to work part time. I am 58.

Is there any way to access my super at 60 as I have already made the employment change usually needed to trigger access?

To access your super in full, you need to have reached preservation age (which is now 60 for everyone) and either of the following happens:

- Gainful employment comes to an end AFTER age 60, or

- Gainful employment has come to an end in the PAST and you do not intend to be gainfully employed (working more than 10 hours a week) again.

If you are still working at age 60 (“gainfully employed”), you cannot fully access your super.

You can still access the “transition to retirement” provisions from age 60 though. This strategy lets you start a pension with your super with the only restriction being the maximum you can take out is 10 per cent of your balance each financial year.

Craig Sankey is a licensed financial adviser and head of Technical Services and Advice Enablement at Industry Fund Services.

Disclaimer: The responses provided are general in nature, and while they are prompted by the questions asked, they have been prepared without taking into consideration all your objectives, financial situation or needs.

Before relying on any of the information, please ensure that you consider the appropriateness of the information for your objectives, financial situation or needs. To the extent that it is permitted by law, no responsibility for errors or omissions is accepted by IFS and its representatives.

Want to see more stories from InDaily Qld in your Google search results?

- Click here to set InDaily Qld as a preferred source.

- Tick the box next to "InDaily Qld". That's it.